The Evolution of US Option Trading: A Five-Year Analysis

A descriptive analysis of the evolution of US option trading from April 2021 to April 2026, using intraday large option flow data spanning 1,253 trading sessions, 5,509 unique tickers, and 188 million large orders representing $12 trillion in premium. We document sustained growth in trading activity, rising multi-leg strategy usage, and a dramatic shift toward shorter-dated options—especially 0DTE.

1,253

Trading Sessions

5,509

Unique Tickers

188M

Large Orders

$12T

Total Premium

Key Findings

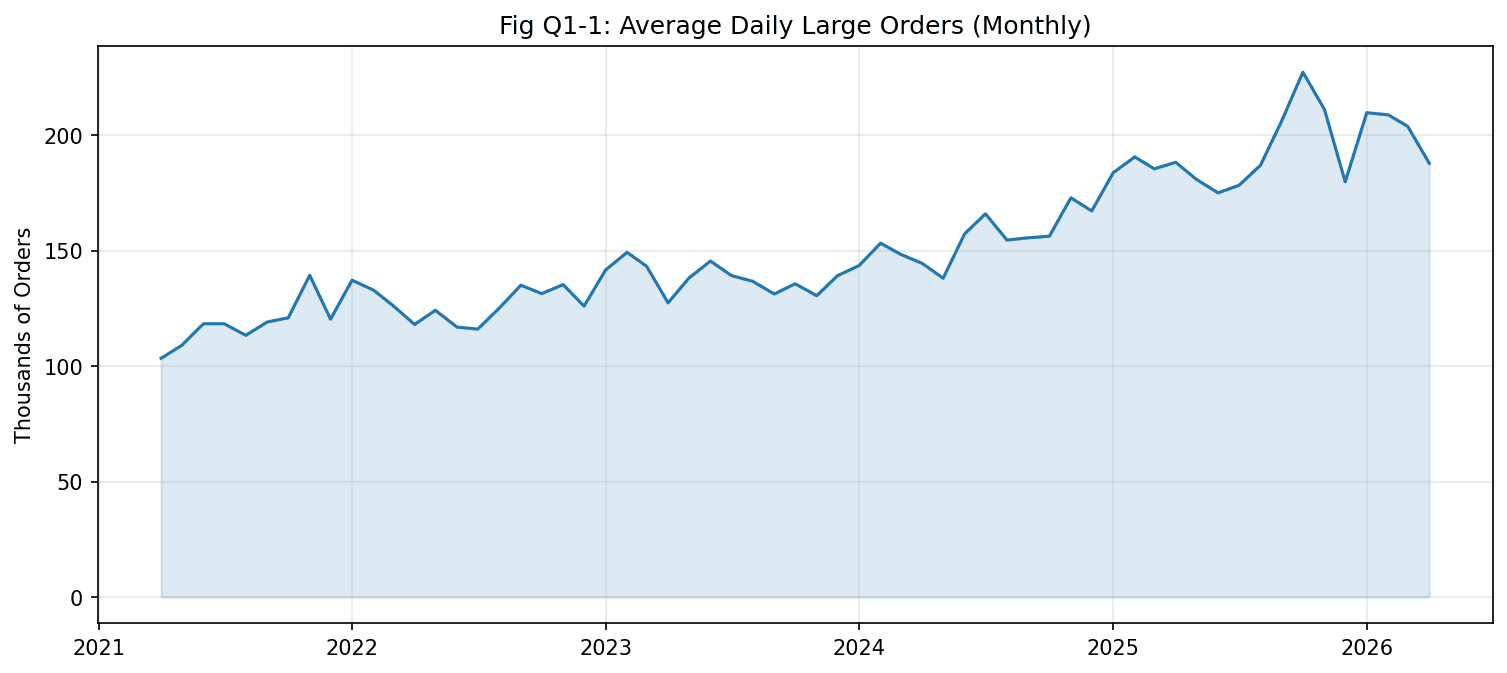

Activity Growth

Large-order activity approximately doubled from ~100,000 to over 200,000 daily orders between 2021 and 2026, with aggregate premium flows growing even faster as average trade sizes increased.

Figure 1 — Average daily large orders (50+ contracts) grew from ~100K in mid-2021 to over 200K by early 2026.

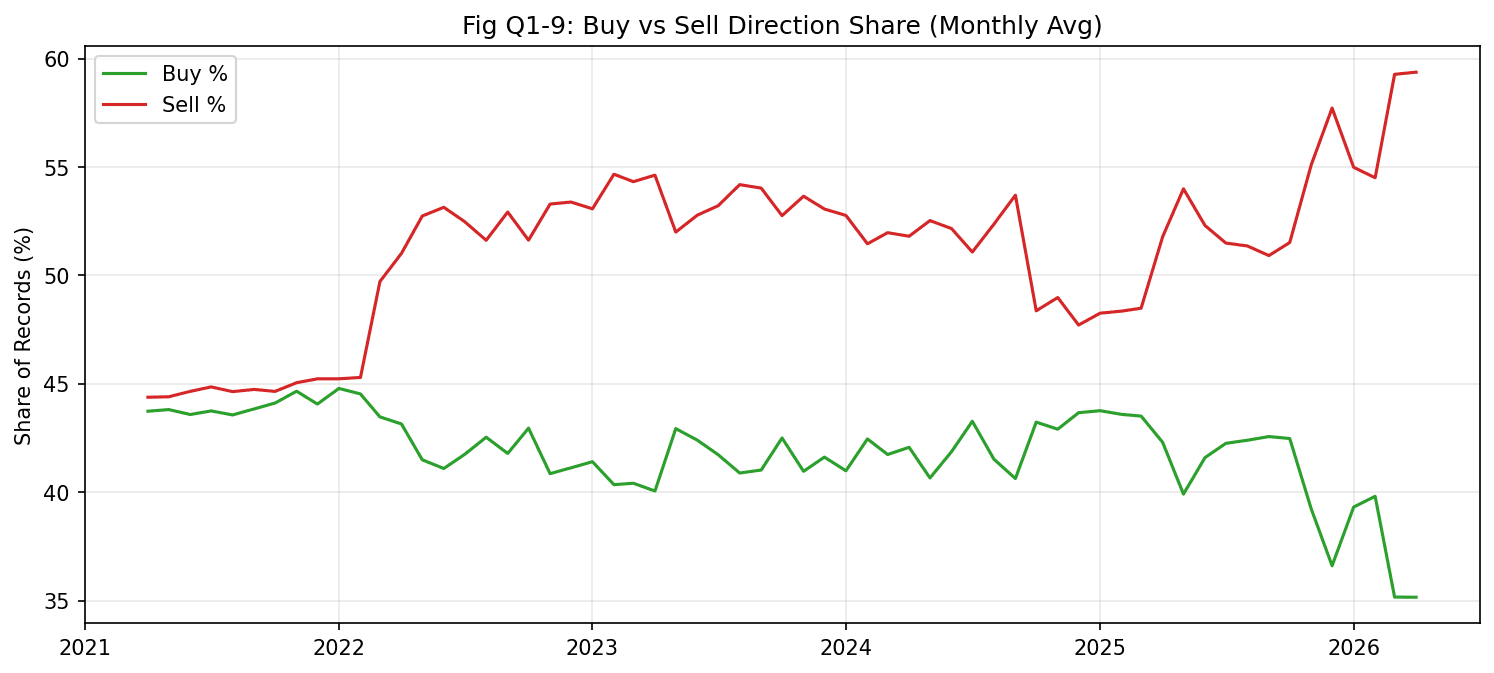

Directional Composition Shift

Sell-initiated large orders steadily gained share over buy-initiated orders, potentially reflecting the growth of premium-selling strategies such as covered calls and credit spreads among institutional participants.

Figure 2 — Sell-labeled flow gained share over the sample period, crossing above buy share by 2024.

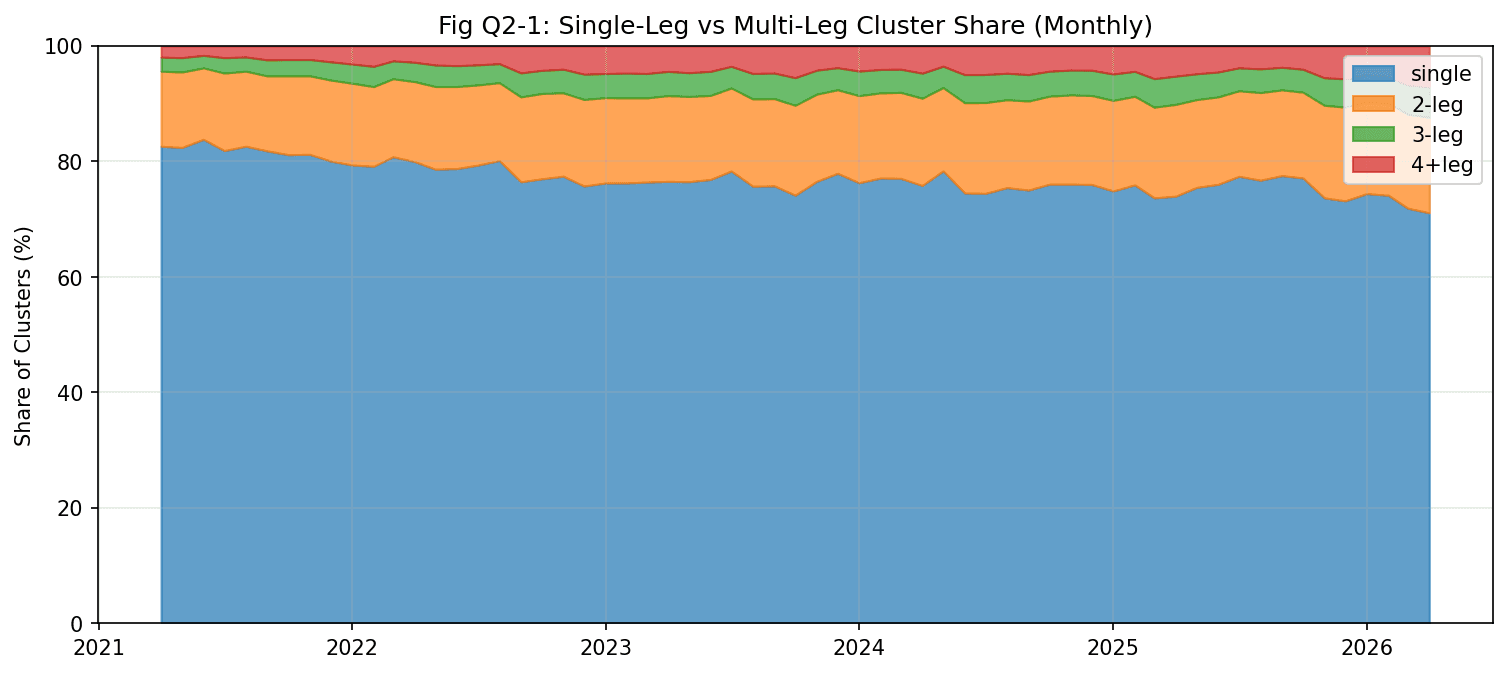

Strategy Sophistication

Multi-leg order clusters—inferred from same-second execution grouping—grew in share, suggesting increased use of defined-risk structures such as vertical spreads, straddles, and iron condors.

Figure 3 — Multi-leg clusters (2-leg, 3-leg, 4+) expanded their share of total order flow over time.

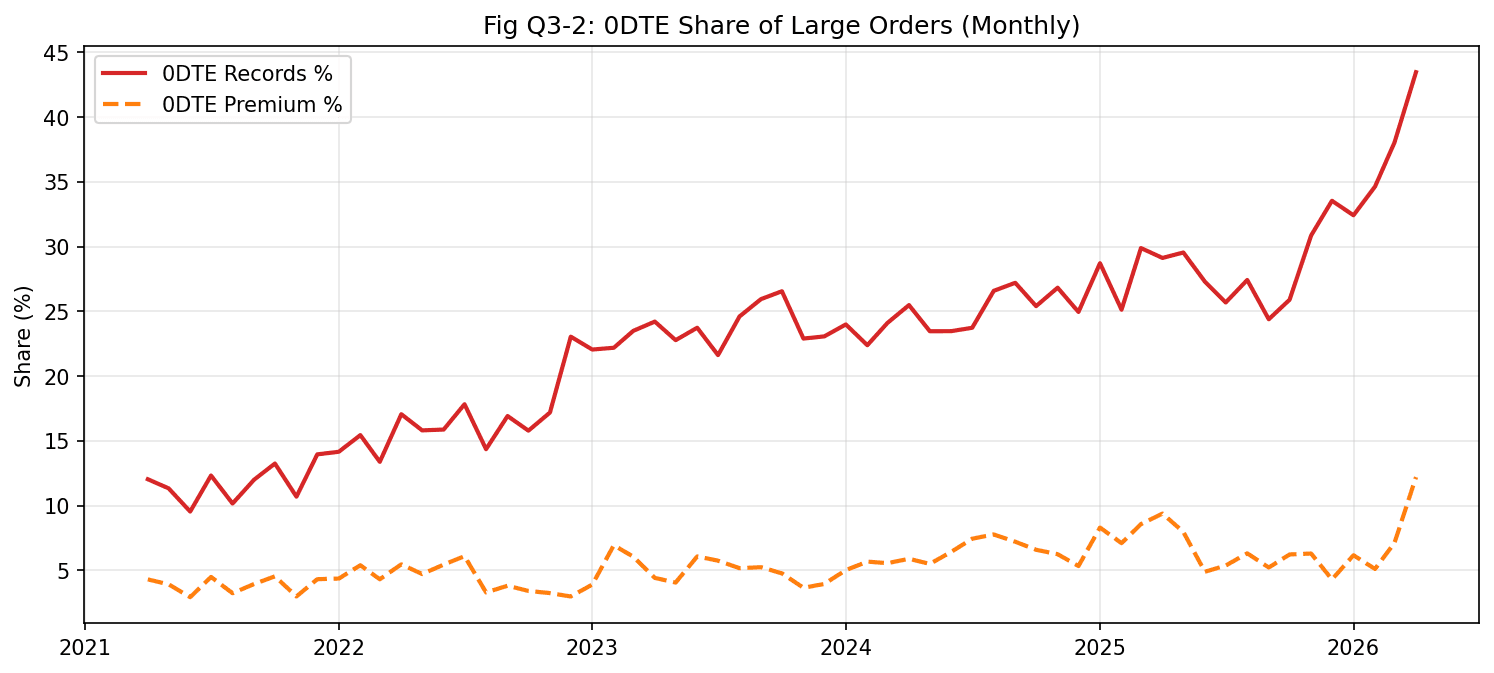

The 0DTE Revolution

Zero-days-to-expiration options rose from roughly 12% to over 40% of all large orders—the paper’s single strongest finding—driven by the introduction of daily expirations on major index ETFs.

Figure 4 — 0DTE share of large order records surged from ~12% in 2021 to over 40% by 2026.

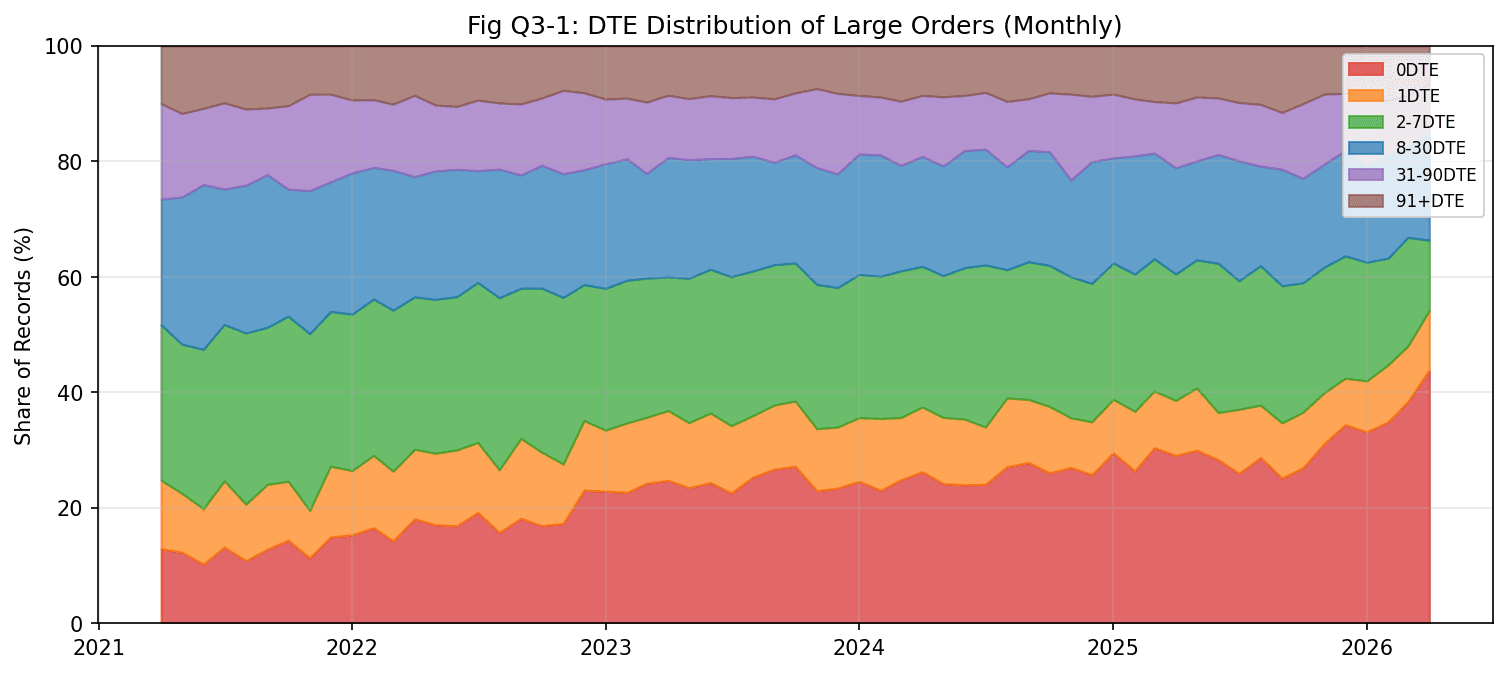

Maturity Compression

The entire DTE distribution shifted toward shorter maturities, with 0DTE and 1DTE now representing more than half of all large orders. Longer-dated contracts (30+ DTE) saw their share decline correspondingly.

Figure 5 — The stacked DTE distribution shows a broad structural shift toward shorter-dated contracts.

Data & Methodology

Analysis of intraday large option flow (50+ contracts) from 2021-04-08 to 2026-04-07 across 1,253 trading sessions. Strategy complexity is inferred from same-second order clustering. All data sourced from optionwhales.io proprietary flow collection infrastructure. See the full paper for complete methodology, classification details, and limitations.

Access the Data

The data behind this research is available through the OptionWhales platform. Track real-time large option flow, inferred strategies, and directional signals across every US-listed equity and ETF.

Continue reading